Memoryless Property (sometimes informally called memorylessness). Both are understood, but “memoryless property” is the more formal and widely used term in academic writing.

The memoryless property is a unique and fascinating concept in probability theory. It describes a situation where the future behavior of a random process does not depend on its past.

In simpler terms:

“What happens next is independent of what has already happened.”

This idea may sound counterintuitive at first, especially in real life where history often matters. But in certain probability models, the past truly has no effect on the future.

Formal Definition

A random variable X is said to be memoryless if:

P(X>s+t | X>s) = P(X>t)

What does this mean?

- The probability that the event lasts at least s+t given that it has already lasted s.

- is exactly the same as the probability that it lasts at least t from the beginning.

The “clock resets” after time s.

Distributions That Have the Memoryless Property

Only two probability distributions possess this property:

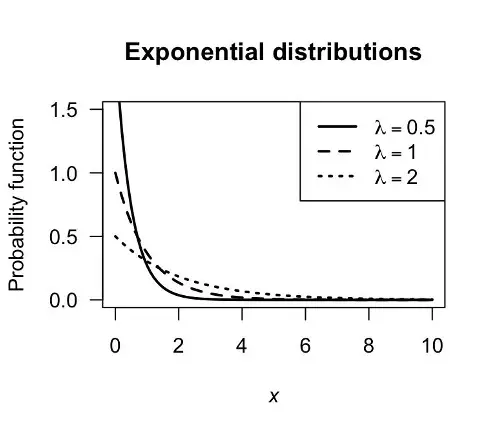

1. Exponential Distribution (Continuous)

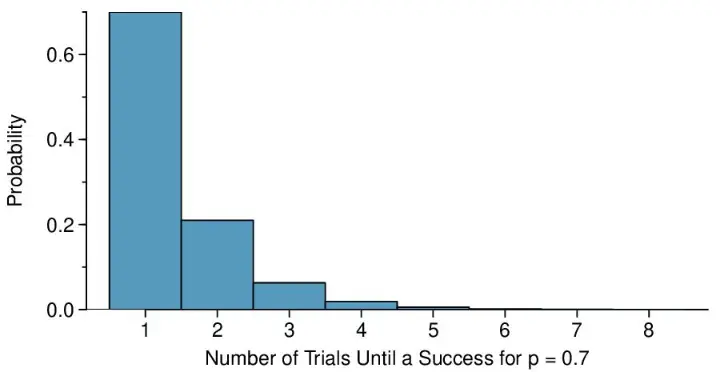

2. Geometric Distribution (Discrete)

1. Continuous Case:

Exponential Distribution

The exponential distribution models waiting time between events in a continuous-time process.

Examples:

- Time until a machine fails

- Time between customer arrivals

- Time until the next trade signal in a Poisson-based model

Key Insight:

No matter how long you’ve already waited, the probability of waiting longer remains the same.

2. Discrete Case: Geometric Distribution

The geometric distribution models the number of trials needed to get the first success.

Examples:

- Number of coin flips until the first heads

- Number of trades until first profitable trade

- Number of attempts before a system triggers

Key Insight:

Even after many failures, your chance of success on the next trial remains unchanged.

Why is the Memoryless Property Important?

1. Simplifies Modeling

It removes the need to track history—perfect for:

- Queueing systems

- Reliability analysis

- Algorithmic trading simulations

2. Foundation of Poisson Processes

The exponential distribution is deeply tied to Poisson processes, widely used in:

- Financial modeling

- Event-driven systems

- Network traffic analysis

3. Real-World Interpretation

It helps model systems where:

- Events occur randomly

- There is no “aging” or “learning” effect

When Memorylessness Does NOT Apply? 🚫

Most real-world processes are not memoryless.

Examples:

- Human learning (experience matters)

- Mechanical wear and tear (aging increases failure probability)

- Financial markets with trends and volatility clustering

👉 In these cases, past information does influence future outcomes.

Intuition Through Example

Imagine you are waiting for a bus that arrives randomly:

- You’ve already waited 20 minutes

- What’s the chance you’ll wait 10 more minutes?

If the process is memoryless:

It’s the same as if you had just arrived at the bus stop.

This feels strange—but it’s exactly how exponential waiting times behave.

Mathematical Insight

The memoryless property is so restrictive that:

- In continuous distributions → only the exponential distribution satisfies it

- In discrete distributions → only the geometric distribution satisfies it

This makes it a rare and powerful property in probability theory.

Conclusion

The memoryless property (or memorylessness) is a cornerstone concept in probability that highlights a very special type of randomness—one where history does not matter at all.

Key Takeaways:

- ✔ The correct term is memoryless property.

- ✔ Only exponential and geometric distributions have it.

- ✔ It simplifies modeling by ignoring past events.

- ✔ It is widely used in engineering, finance, and data science.

Understanding the Memoryless Property in Probability Distributions